Home » Resources

Resources

In tracking material topics, some analysts monitor global risks, some assess new regulations, some scan media reports, some recommend key topics by sector, some add up number of company disclosures on select indicators…

Materialitytracker serves as a resource on new studies and standard develoment trends in the field of materiality, considering the needs of financial accountants and sustainability accountants. This section provides an overview of recent reports and background studies, reflecting varied approaches to tracking materiality.

Global Risks (World Economic Forum)

Since 2006 the World Economic Forum (WEF) publishes an annual Global Risks Report. A listing of top global risks reflects the results of a survey among its multistakeholder (>40% business) network of over 700 leaders worldwide. The WEF defines a “global risk” as an occurrence that causes significant negative impact for several countries and industries over a time frame of up to 10 years. Importantly, the focus today is on systemic risk, interconnections between risks and longer term impacts. The reports (see www.weforum.org/issues/global-risks) provide an important barometer for global corporations in determining materiality. From 31 risks covered in its 2014 edition, the following were found to be the ten global risks of highest concern:

- Fiscal crises in key economies

- Structurally high unemployment / underemployment

- Water crises

- Severe income disparity

- Failure of climate change mitigation and adaptation

- Greater incidence of extreme weather events (e.g. floods, storms, fires)

- Global governance failure

- Food crises

- Failure of a major financial mechanism / institution

- Profound political and social instability

The 2015-2017 editions found the following top ten global risks to stand out as both highly likely and potentially highly impactful:

Recommended menus of material issues and KPIs by industry sector (SASB)

Following less of a principles-based and a more rules-based approach, the Sustainability Accounting Standards Board (SASB) in the USA set out to determine menus of material issues and related KPIs by industry sector. Use of these does not relieve senior executives from their responsibilities in disclosing material information in SEC filings. It does however seek to present short checklists to preparers and users, paying less attention to participatory materiality determination process run by companies individually on an ongoing basis. Its point of departure is over 40 sustainability issues that apply across ten clusters of industries. Determining a Materiality Map for each industry cluster is done through a process of tests that consider:

(i) evidence of interest,

(ii) evidence of financial impact, and

(iii) need for forward-looking adjustment (e.g. risk of systemic disruption).

This involves a process similar to that followed by expert analysts based in rating agencies, and has specifically investor needs in mind. The resultant sector standards with lists of Material Topics and Accounting Metrics are available at: www.sasb.org/standards/download/

Recommended issues and KPIs by industry sector (GRI)

Industry sector supplements have been developed under GRI auspices with multistakeholder involvement since the early 2000s. These provide additional indicators for topics felt to be particularly relevant for different industry sectors. Currently ten G4 sector disclosures are available at: www.globalreporting.org/reporting/sector-guidance/sectorguidanceG4/Pages/default.aspx

As an example, the GRI Sector Supplement for the Financial Services sector includes content that has been added to the Aspects of economic performance, emissions, effluents and waste, occupational health and safety, investment, local communities as well as product and service labeling. Finance sector specific Aspects added are Product Portfolio, Audit and Active Ownership. Examples of finance sector specific Indicators added are “Acces points in low-populated or economically disadvantaged areas by type” and “Monetary value of products and services designed to deliver a specific social benefit for each business line broken down by purpose”.

Mandatory and Voluntary Disclosure Requirements Worldwide

The Carrots and Sticks series by UNEP, GRI, KPMG and the Centre for Corporate Governance (USB) provide an overview of mandatory and voluntary requirements for disclosure of sustainability information by companies in OECD and emerging market countries. Legislative or regulatory requirements to disclose information on subjects such as employment diversity and climate change predetermine some content to be part of annual reporting. The 2006, 2010, 2013 and 2016 editions of Carrots and Sticks can be found below (PDF links):

- Carrots & Sticks I – 2006

- Carrots & Sticks II – 2010

- Carrots & Sticks III – 2013

- Carrots & Sticks IV – 2016

The new EU Directive 2014/95/EU on the disclosure of non-financial and diversity information by large enterprises (> 500 employees) in Europe gives indication of an expanded menu of issue areas that regulators felt should be reported on “to the extent necessary” (including principal risks and KPIs). These “categories” and “topics” are environmental matters, social and employee aspects, respect for human rights, anticorruption and bribery issues, and diversity in the board of directors. The Carrots and Sticks series also signals the trend in emerging markets that has been for stock exchanges to introduce self-regulatory requirements for comprehensive sustainability disclosure. See the Carrots and Sticks database online at: www.carrotsandsticks.net

Analysis of published reports (e.g. by GRI, RobecoSAM, Governance and Accountability Institute)

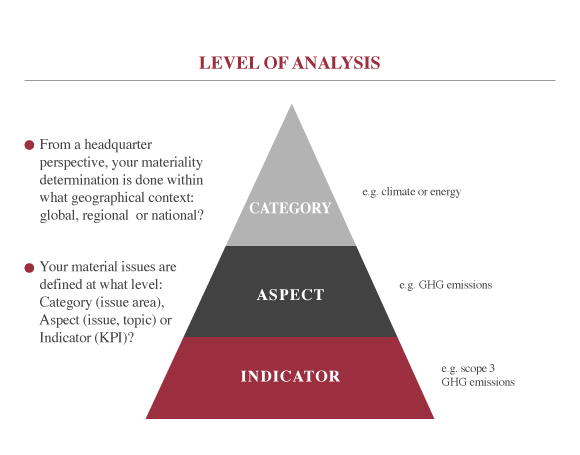

Analysis of published reports to identify top material topics reported on reflects two approaches (see “Level of Analysis” image below). One is focussed more broadly at the level of categories and aspects or topics within them. The other delves a level deeper and focuses on aspects or topics and indicators related to them that are most reported against. An example of the former is the study Defining Materiality: What Matters to Reporters and Investors (2015) published by GRI and RobecoSAM. It examined 39 reports of the Technology Hardware & Equipment sector, as well as 94 reports of the Banks & Diverse Financials sector. The reports were selected from the GRI online database (publication year 2013). For the financial sector, it found the following to be the top 10 GRI Aspects reported on:

- Community (local community)

- Training and Education

- Product and Service Labelling

- Product Portfolio

- Economic Performance

- Employment

- Emissions, Effluents and Waste

- Diversity and Equal Opportunity

- Compliance

- Customer Privacy

For its Materiality – What Matters? (2014) study, the Governance & Accountability Institute (New York) examined 1246 reports from 35 economic sectors. These were also selected from the GRI reports database (publication year 2012). Its methodology includes the “out-weighing” of generic topics so that sector-specific topics stand out more clearly. Illustrative of its more specific focus, it found the following to be the top 10 GRI indicators reported on by the financial sector:

- Programmes for adherence to laws, standards and voluntary codes related to marketing communications (Product Responsibility)

- Volume of significant investment agreements that include Human Rights clauses (Human Rights)

- Significant indirect economic impacts (Economic)

- Total number of substantial complaints regarding breaches of customer privacy and losses of customer data (Product Responsibility)

- Percentage of materials used that are recycled input materials (Environment)

- Practices related to customer satisfaction (incl survey results) (Product Responsibility)

- Materials used by weight or volume (Environment)

- Coverage of the organisation’s defined benefit plan obligations (Economic)

- Total value of financial and in-kind contributions to political parties (Society)

- Range of ratios of standard entry level wage compared to local minimum wages (Economic)

For more information and access to the above studies, see www.robecosam.com/en/sustainability-insights/library/study.jsp and www.ga-institute.com/research-reports/research-reports-list.html.