In a 2011 ESG brief the Canadian Institute of Chartered Accountants (CICA) stated one of the key questions board directors should ask:

“Are we satisfied with management’s assessment of the financial impacts of key environmental and social issues and related regulations on performance, liquidity and financial condition?” This suggests key interest in how environmental, social and governance (ESG) issues affect the (financial) performance of the organization. Is a demonstrative (past / present / future) link with “financial” essential?

In following the Six Capitals model, the IIRC refers to the materiality decision as having to consider impact on one or more of the capitals the organization uses or affects. It can be argued that for a commercial enterprise, Financial Capital is inevitably at the heart of this. It represents the common currency that translates impacts or dependencies on all other capitals into business relevant information.

Even if a shared value approach is pursued, inevitably the lens through which the managers and owners of the business approach materiality is the performance and financial health of the reporting organization itself. Furthermore, if an environmental expert therefore views a certain environmental externality as material but an investor disagrees, the onus is on the former to point to actual or likely impact of the said externality on the financial performance of the organization in the short, medium or long term.

Does this imply that defining a clear link between a sustainability or social responsibility issue and corporate financial performance is a precondition for the issue being considered material? It would certainly be odd if a link with its financial performance cannot be defined (at least in convincing qualitative terms where cause-and-effect quantitative data is not immediately available). The more critical question is whether that link refers to financial impact and financial health in the short, medium or longer term. The strategic approach to materiality certainly takes a longer-term view.

Would thresholds applied to ESG issues also be financial? Would financial accounting thresholds commonly applied be appropriate to reflect the seriousness of ESG issues, putting it in proper context? Take for example the case of a company breaching by 5% the extracted level of freshwater allowed in terms of its license agreement. Should the threshold be whether the metric volume is breached by 5% or 10%, or whether the resultant fine or penalty enforced by the regulator results in a cost of 5% or more of net income? Since regulations seldom ensure the appropriate pricing of natural resources, how practical is the use of a financial accounting threshold?

Also, considering who should be doing the calculations and judgment involved, what relevant experience and educational background should the auditor or assurance provider have? Can the financial accountant show sufficient understanding of the ESG issue involved? Can the sustainability accountant involved show sufficient understanding of the corporate finance dynamics involved?

In the 2000s, AccountAbility identified the first materiality test as being “direct short term financial impacts“. This was described as being typical of classical, narrow approaches to interpreting materiality. A key shift in applying materiality in a more strategic way today involves considering (i) “direct and indirect” as well as (ii) “long(er) term” financial impact. More inclusive and complex approaches involve looking also at non-financial impacts, and (to greater or lesser degree) in how far they have financial consequences for the reporting business.

An approach that emphasizes the link with financial performance information considers core financial value drivers. These have been defined during the 1980s as key variables for shareholders. They are:

- Growth of sales,

- Duration of sales,

- Operating margin,

- Investment in fixed capital,

- Investment in working capital,

- Tax rates, and

- Cost of capital.

These are the type of value drivers that the IIRC expects senior management to refer to in determining relevant matters. The IIRC Background Paper on Materiality (2013) refers to (i) financial value drivers, (ii) other drivers such as customer relations, societal expectations, environmental concerns, innovation and corporate governance, and (iii) values such as integrity, trust and teamwork that support value creation. Value drivers alone and in combination affect an organization’s ability to create value over time.

Some with good reason question an overemphasis on making the link with financial consequences. Some ESG issues have materiality on their own terms. Yet in the absence of adequate regulations (that serve to internalize externalities), sustainability topics often fall outside the parameters of the asset or liability recognition criteria of probable future economic benefit or cost that can be measured reliably. These criteria of the accounting principle of ‘recognition’ have traditionally left many ESG topics out in the cold as far as materiality is concerned.

Yet new perspectives on “the public interest” and “trust in capital markets” since the 2000s are leading to a change in approach. In recent years regulators have determined that issues such as involvement in illegal activity (cf conflict minerals) or governance characteristics are material for investors to know, irrespective of their “financial materiality”. These point to potentially significant risks and opportunities.

An overemphasis on financial consequences, notably if obsessed with the direct and short term, also leads to lack of strategic insight. This is what the Initiative for Responsible Investment at Harvard University referred to when recommending the use of three principles for determining materiality. A sustainability factor is likely to be more material if (i) it has the potential to cause disruption, (ii) if the degree of uncertainty or unpredictability of the disruption is greater, and (iii) if the disruption is likely to take place over a longer term. These principles are applied by SASB in compiling industry sector Materiality Maps. It applies three tests of which the second is “Evidence of Financial Impact”.

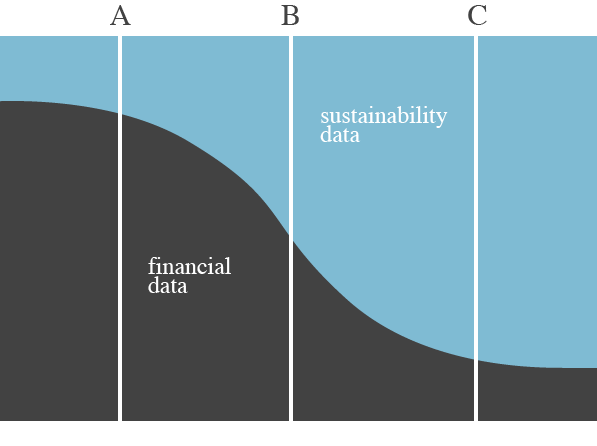

The total mix of information considered by the user of published statements or reports will therefore contain different levels and combinations of financial and non-financial or sustainability data related to issues A, B, C, etc. (see graphic below).

Material information involves not only historical data (i.e. financial performance data) but also forward-looking information including projections or forecasts. The IIRC has argued that it is not necessarily intended that organizations be required to disclose forecasts or projected results. Rather, they should simply disclose the material raw information that would enable investors and other stakeholders to run models or make their own predictions about the future value creation potential of the organization. Aware that legal or regulatory requirements may apply to certain future-oriented information, the IIRC IR Framework states that future-oriented information is by nature more uncertain than historical information. Uncertainty is not, however, a reason in itself to exclude such information from reporting.

Considering the risk of providing proprietary information to competitors, companies would normally not be required to disclose sensitive information related to for example trade and R&D programmes. Both GRI and IIRC expect that if material information is not disclosed because of perceived competitive harm, this fact and the reasons for it will be noted in a report.