Little guidance on thresholds can be found in non-financial accounting and assurance standards issued since the 2000s…

This includes standards such as AA1000, ISAE3000 and issue-specific standards such as the GHG and water accounting standards issued by ISO and the Water Accounting Standards Board. The seemingly limited guidance on quantitatively determining the materiality of non-financial or ESG issues have led some to suggest that qualitative factors are more likely to be considered in these cases. In how far does a social agenda lend itself to defining quantitative thresholds related to the impact of business operations?

Qualitative factors may include the possible contravention of the law or breach of a contract if a compliance-driven, legalistic approach is followed. It could also include the seriousness and salience of a socio-economic or environmental problem faced by the reporting organization in its operational or local community context. The extent of the problem may be confirmed by both qualitative and quantitative information, more or less linked to the operations of the reporting organization itself.

Can traditional thresholds applied in financial accounting be applied to non-financial, sustainability information? In how far will their application be different when the “user” (beholder) is not the investor but other financial stakeholders, or the comprehensive range of societal stakeholders (internal and external to the firm)? Is it even possible to define thresholds to determine the materiality of some ESG issues or events? Consider that many ESG items do not have a market price that can be referred to. In the case of some issues the definition of a threshold may even be inappropriate, for example child labour or employee fatalities, where the occurrence of just one instance is likely to be material from a moral-ethical, social license and reputational risk point of view.

Sustainability experts increasingly emphasize the need to convey performance in context and define science-based targets. In doing so, they focus on thresholds that refer not to financial accounting metrics but to the condition of ecology and society within which the business operates. It has for example been argued that sustainability requires contextualization within thresholds. The type of thresholds referred to are often environmental ones, employing concepts such as “critical loads”, “tipping points”, “ecological carrying capacity” or the nine “Planetary Boundaries” as defined recently by Swedish scientists (www.stockholmresilience.org).

What practical methodologies are there for companies to use in setting sustainability performance targets with reference to recognized sustainability thresholds? The most likely action areas with ready tools are carbon and water footprinting or accounting, defined with the use of standards of the WRI/WBCSD, Water Footprint Network, Global Footprint Network and International Organisation for Standardisation (ISO).

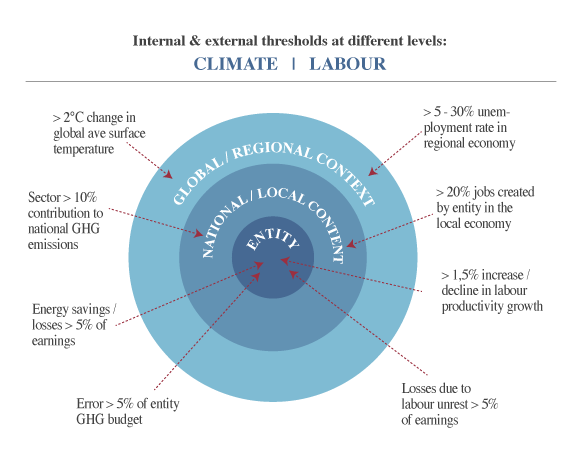

The GHG Protocol of the WRI/WBCSD argues that as a rule of thumb, an error is considered to be materially misleading if its value exceeds 5 percent of the total inventory for the part of the organization being verified. It adds that the verifier needs to assess an error or omission in context. For example, if a 2 percent error prevents a company from achieving its corporate target, this would most likely be considered material. From this guidance in the GHG Protocol it is evident that there are two types of sustainability thresholds (see image below):

- Sustainability thresholds that are internal (organizational performance thresholds); and

- Sustainability thresholds that are external (ecological thresholds and socio-economic thresholds).

Even if environmental thresholds were to be defined perfectly scientifically, the imperfections of market information, pricing of externalities and imperfect knowledge of financial decision-makers still leave plenty of room for surprise. If further scientific thresholds and methods were to be defined for organizations to set themselves science-based targets, one point of departure may be the ecological planetary boundaries, requiring thresholds related to not only climate but also ozone depletion, biodiversity degradation, chemicals use, freshwater use, land use, ocean acidification and the nitrogen cycle. The status related to these and country allocations of responsibilities for improvement are addressed under various international environmental conventions associated with the United Nations.

What “sustainability thresholds” would apply in the social domain, say Human and Social Capital? These may be quantitative references such as socio-economic conditions (for example levels of poverty and inequality by country, levels of unemployment by country, levels of health with respect to globally critical illnesses such as AIDS, tuberculosis, malaria and obesity by country) in the regions and countries where reporting companies operate. In some cases organizations may need to refer to qualitative references in the absence of reliable quantitative data. Considering shortlists of key material topics of a company, defining socio-economic thresholds need not be rocket science. Consider the country studies with economic and risk data that corporations refer to when assessing their risk profile and markets they operate in globally.

Based on the “materiality tests” recommended by voluntary standards initiatives such as the GRI, AccountAbility and SASB, the folowing types of integrated sustainability thresholds can be considered with reference to both the internal and external context of the reporting enterprise:

- % level of short / medium / long term financial impact (e.g. on revenues, profitability and capital efficiency)

- # level of risk (probability, magnitude and timing) identified by experts / scientists

- % of stakeholders (prioritised category/ies) showing interest / concern

- % number of peers / competitors considering it material

- # level of matureness of the issue, from emerging to being incorporated into laws and regulations

- % of managers / executives showing interest / concern